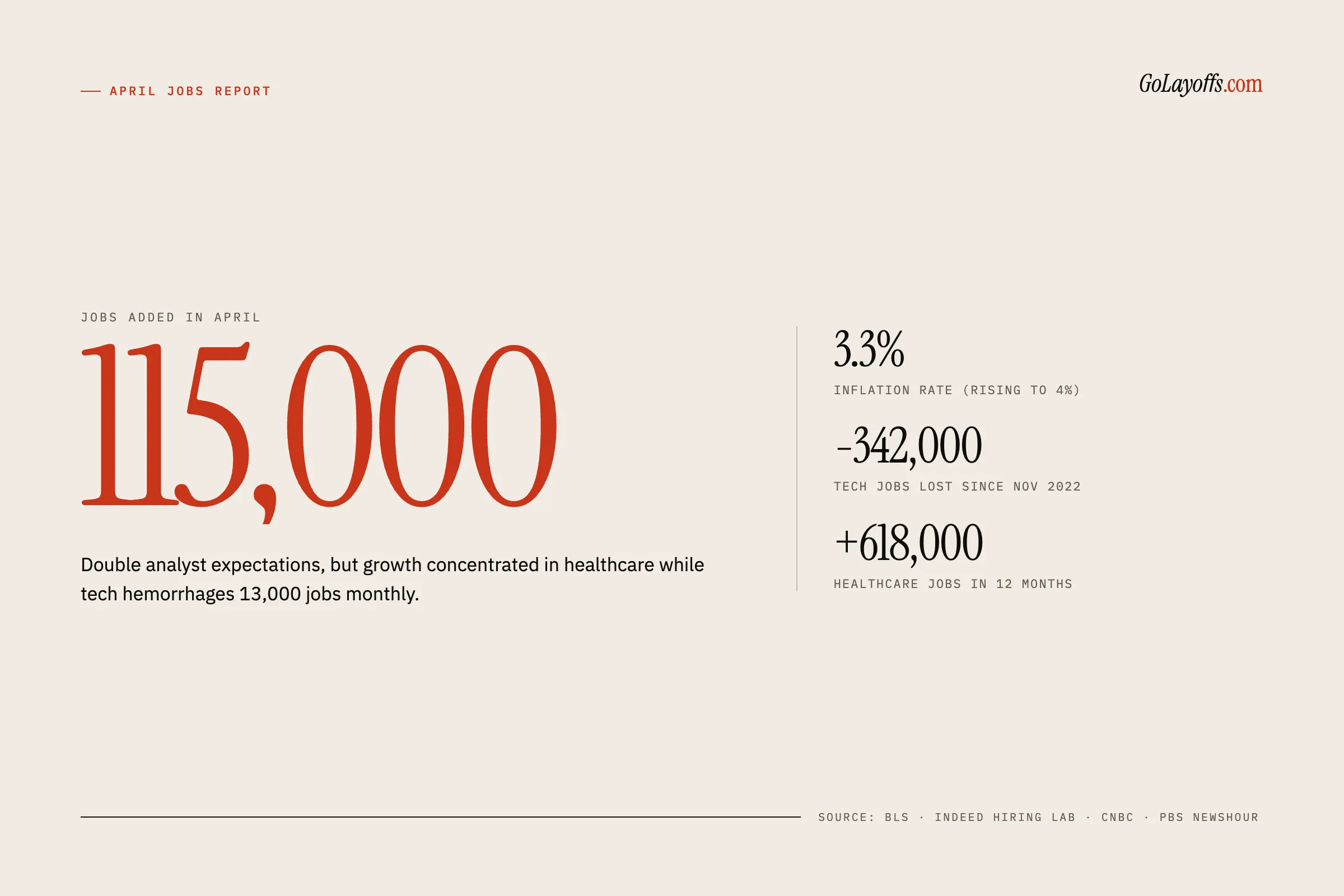

The United States added 115,000 jobs in April 2026, double economists’ expectations and the second consecutive month of growth. But behind the figure that surprised Wall Street lies a much more complex reality: inflation is running at 3.3%, the tech sector has lost jobs for the sixteenth consecutive month, and the Federal Reserve is running out of reasons to cut interest rates. For American workers — and by extension European ones — the labor “boom” hides a silent erosion of purchasing power.

Key points:

- 115,000 jobs added: nearly double the 62,000 expected by LSEG.

- Unemployment rate: steady at 4.3%, unchanged for months.

- Inflation: at 3.3% (and expected to reach 4% in coming months), well above the Fed’s 2% target.

- Wages: +3.6% annually, but eroded by inflation and gasoline prices above $4.50/gallon.

- Tech in crisis: -13,000 jobs in the “information” sector, with 342,000 lost since November 2022.

- Healthcare saves the day: +37,000 jobs, 618,000 over the last 12 months.

- Fed stuck: markets are pricing in zero rate cuts until April 2031.

Official data from the Bureau of Labor Statistics, published on May 8, 2026, show a labor market that — as economist Indeed Hiring Lab Cory Stahle summarized — is “moving, but not advancing.”

115,000 Jobs, but Is It Really a Recovery?

The Official Department of Labor Numbers

The Bureau of Labor Statistics report, released Friday, May 8, surprised virtually everyone. Of the 100 economists surveyed by Bloomberg, 94% had predicted a worse result. LSEG’s consensus estimate stood at 62,000 jobs; Dow Jones had gone as high as 55,000. The final number was nearly double.

Acting Secretary of Labor Keith Sonderling commented on the release with a statement emphasizing the Trump administration’s achievements:

115,000 jobs were added in April, doubling expectations and proving 94% of Bloomberg economists wrong. The unemployment rate remained stable, and total private-sector job growth under this administration has now surpassed 700,000 new jobs.

Sonderling attributed the result to the “Working Families Tax Cuts” signed by Trump, highlighting in particular manufacturing growth (+5.2% year-over-year in weekly wages) and construction. The reality, however, is more nuanced: April’s data comes after March was revised upward to +185,000 jobs, but also after February was revised downward to -156,000 jobs (a negative revision of 23,000 units). Combined February and March employment is now 16,000 jobs lower than initially reported.

.@POTUS on the blockbuster April jobs report: “We have more people working today than we ever had working in this country. The job numbers today were incredible.” pic.twitter.com/bBNL2hug2t

— Rapid Response 47 (@RapidResponse47) May 8, 2026

The overall picture is therefore this: after a 2025 in which average monthly growth had been anemic (10,000 jobs per month), 2026 is showing an average of 76,000 jobs — a clear improvement, but still well below the psychological threshold of 100,000.

Historical Comparison: 2024 vs 2025 vs 2026

Putting the data into historical perspective, the scale of the slowdown becomes evident:

- 2024 (monthly average): ~165,000 jobs added per month

- 2025 (monthly average): ~10,000 jobs added per month (the “hiring recession”)

- 2026 YTD (monthly average): ~76,000 jobs added per month

As Eva Roytburg summarized on Fortune, “economists are beginning to wonder whether the ‘hiring recession’ of the last two years is finally ending.” For much of the labor market, the answer appears to be yes. But the devil, as always, is in the details.

The Inflation Trap: Wages Rise, but Purchasing Power Falls

Here comes the first major paradox. Average hourly wages increased by 3.6% year-over-year, reaching $37.41/hour. It sounds like good news, until you look at inflation: in March 2026, the Consumer Price Index hit 3.3%, a two-year high, and analysts estimate it could reach 4% in the coming months due to the war with Iran and gasoline prices above $4.50/gallon.

Translated: real wages are about to return to negative territory. As Roytburg herself wrote in a later analysis, “Americans still have jobs, but they are being financially crushed by rising gasoline and transportation costs.”

The sharpest analysis comes from Mohamed El-Erian, professor at the Wharton School and chief economic advisor at Allianz, interviewed on PBS NewsHour on May 8. El-Erian identified three critical points:

Job creation, double expectations, showed very strong labor demand, even though we have thrown everything at this economy. The labor market remains resilient. But on the labor supply side, there are challenges. We have seen labor force participation decline and the labor force itself shrink.

El-Erian emphasized how the apparently positive data hides a contraction in participation: fewer people are looking for work, and the broader unemployment rate (the so-called U-6, which includes discouraged and involuntary part-time workers) rose to 8.2%.

The Invisible Divergence: Which Sectors Are Actually Growing?

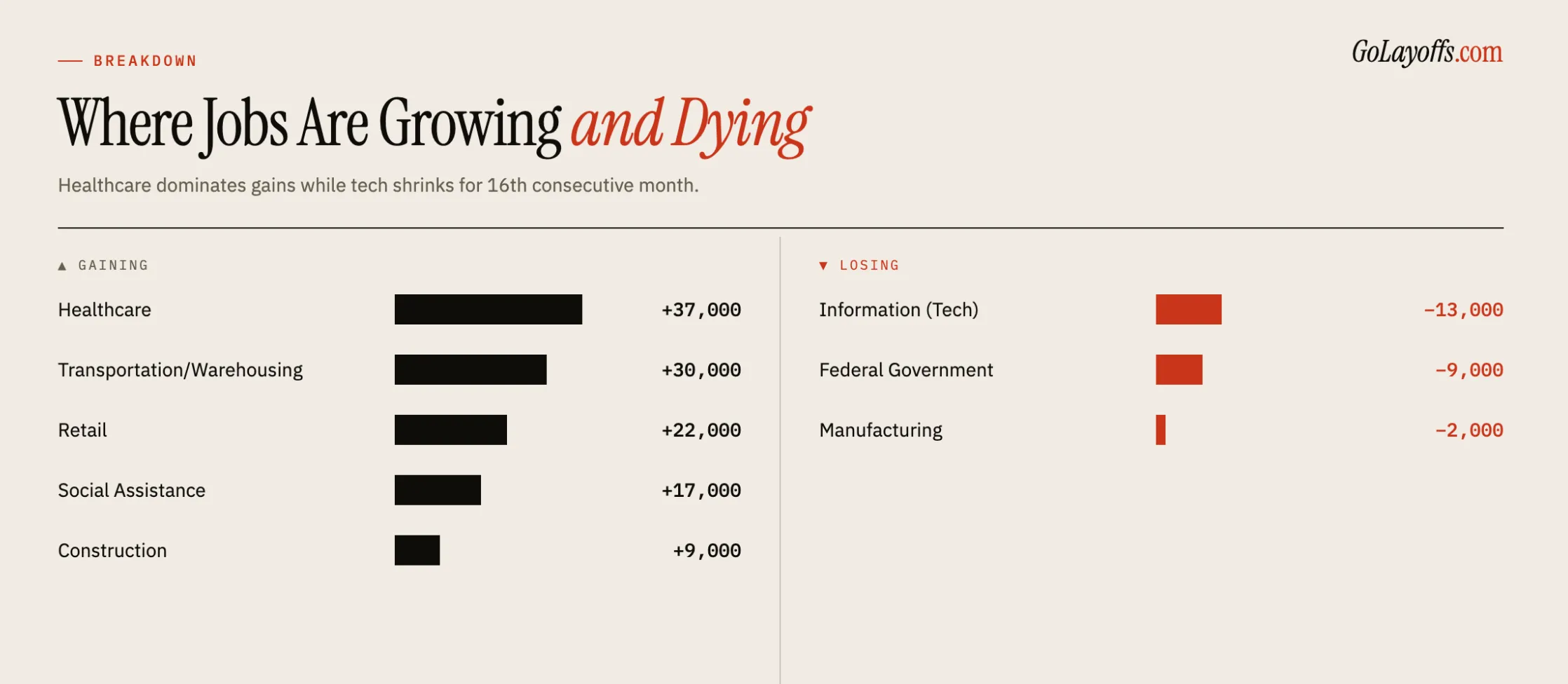

The aggregate figure of +115,000 jobs hides dramatic divergences between sectors. Here is the real breakdown:

Growing sectors:

- Healthcare: +37,000 (in line with the 12-month average of +32,000)

- Transportation and warehousing: +30,000 (driven by couriers and messengers: +37,900)

- Retail: +22,000 (driven by department stores)

- Social assistance: +17,000

- Construction: +9,000

Sectors in decline:

- Information (tech, telecom, media): -13,000

- Federal government: -9,000 (continued effect of DOGE cuts)

- Manufacturing: -2,000 (-66,000 over the last 12 months despite protectionist policies)

Indeed Hiring Lab figures make the picture even more striking: over the last 12 months, healthcare employment grew by 618,000 jobs, while all other sectors combined lost 367,000 jobs. In other words, without healthcare, America would be in a full employment recession.

Tech Loses 13,000 Jobs but Invests $725 Billion in AI: The Great Contradiction

The Numbers Behind the Tech Collapse: 16 Consecutive Months of Losses

The “information” sector — which includes tech, telecommunications, digital media, motion picture, and cloud — has lost jobs for the sixteenth consecutive month. Since November 2022, coinciding with the explosion of ChatGPT and generative artificial intelligence, the sector has lost 342,000 jobs in total, 11% of its overall workforce.

Layoffs continue to hit the industry giants: Amazon announced 30,000 corporate cuts between October 2025 and January 2026 (the largest restructuring in its history), and Meta, Google, and Microsoft followed similar trajectories. As Cory Stahle summarized to Marketplace on NPR:

What we are seeing in IT and tech right now is really a restructuring. These layoffs are… cut here so they can spend the money on AI over there.

The AI Paradox: $725 Billion in Investments, Zero New Jobs

Here lies the great contradiction of 2026. The four American hyperscalers — Google, Amazon, Meta, Microsoft — will collectively invest more than $725 billion in AI capex in 2026 alone, with Amazon leading at $125 billion. Yet these astronomical figures are not translating into jobs. As Stahle explained:

Even though many of those hundreds of billions of dollars are going toward steel and silicon rather than personnel.

Data centers are highly automated. New AI jobs go to a very narrow elite of specialized engineers — AI/LLM engineers who, according to industry data, find jobs within 1–3 weeks at startups like Anthropic or Google DeepMind — while traditional program managers, designers, and engineers face job searches lasting 9–12 months.

The testimony of Joanelle Cobos, a Design Manager laid off by Amazon, is emblematic:

My job search feels like a ticking time bomb.

For many former Amazon and other Big Tech employees, transitioning to mid-market companies means a base salary reduction of between $40,000 and $60,000 per year, especially in MLOps and SRE roles.

Who Survives in the 2026 Economy?

The emerging picture is that of a two-speed economy. On one side, “non-automatable” sectors — healthcare, construction, logistics, hospitality, education — continue hiring. On the other, cognitive and administrative sectors are being eroded by generative AI.

Indeed Hiring Lab’s analysis is particularly blunt:

The healthcare sector continues to show strength, but that strength is relative: it is staying stable while other sectors slowly erode. Healthcare has been the dominant story of job creation for years now, and it continues to mask deeper weakness elsewhere.

Construction saw a +5.2% year-over-year increase in weekly manufacturing wages, signaling a persistent shortage of skilled labor. But even here, behind the aggregate data, there are struggling subsectors: residential specialists lost 8,900 jobs, offset by non-residential gains (+12,600).

The Fed Will Not Cut Rates: What It Means for Mortgages and Savings

The Fed’s Dilemma: High Inflation + Stable Employment = Tied Hands

The April jobs report arrives at a delicate moment for the Federal Reserve. The central bank has just gone through the late-April FOMC meeting with an 8-4 vote, the highest number of dissents since 1992. The official rate remains in the 3.5%-3.75% range, but within the committee, a civil war has erupted over the future direction.

Jeff Cox of CNBC, on May 8, summarized the situation with the headline making waves across the financial world: “The Federal Reserve is quickly running out of reasons to cut interest rates.” His analysis is surgical:

The jobs report for April provided the latest proof that the central bank’s greatest concern is not a weakening labor market, but rather a cost of living that is becoming increasingly difficult for ordinary Americans to sustain.

The logic is simple but relentless: the Fed cuts rates when it needs to stimulate the economy to avoid unemployment. But if the labor market is stable and inflation is running at more than double the 2% target, cutting rates would further overheat prices. As Lindsay Rosner of Goldman Sachs Asset Management stated:

The Fed will shift its focus toward containing upside inflation risks now that the labor market appears to be back on track.

Kevin Warsh and the Conflict with Trump

The picture becomes even more complicated for Kevin Warsh, appointed by Trump as the new Fed chair following Jerome Powell’s departure. Warsh, a former Fed governor, has always expressed a preference for lower rates and an approach focused on the central bank’s balance sheet ($6.7 trillion) rather than Fed Funds. But with inflation above 3%, selling a rate cut to the market will be extremely difficult. Dan North, senior economist at Allianz, commented:

Warsh really has his hands full with this. He was certainly chosen by Trump because he is probably inclined toward lower interest rates.

Paul Tudor Jones, interviewed by CNBC on May 7, also stated that there is “no chance” Warsh will be able to push the Fed toward cutting rates in the short term.

What the Market Is Pricing In: Zero Cuts Until 2031

The fed funds futures data are remarkable in their implications. According to CNBC and the CME Group FedWatch:

- Probability of a rate cut by 2026: ~0%

- Probability of a rate hike in the next 24 months: 10-15% and rising

- Rate cuts priced in through April 2031: essentially none

As Scott Clemons of Brown Brothers Harriman summarized:

This makes it increasingly clear that the Fed can afford to be as patient as it wants. There is nothing on the economic front requiring it to lower interest rates further.

The Silent Erosion of the Middle Class: Wages Up, Purchasing Power Down

Official Real Wage Data

The April report shows an apparently healthy wage picture:

- Average hourly earnings: $37.41/hour (+0.2% monthly, +3.6% annually)

- Average workweek: 34.3 hours (up 0.1 hours)

- Manufacturing: $30.10/hour, 40.4 weekly hours

But when inflation is running at 3.3% — and expected to reach 4% in coming months — a nominal increase of 3.6% means real wages are in negative territory or, at best, flat. As Eva Roytburg said on Fortune:

The bad news is that inflation is once again eroding wage gains. Wages grew 3.6%. That certainly won’t be enough at a time when inflation is expected to hit 4%.

Stories of Tech Layoffs: When Work Becomes a “Ticking Time Bomb”

Behind the aggregate numbers are individual stories. Joanelle Cobos, former Amazon Design Manager, summarized her situation this way: “My job search feels like a ticking time bomb.” She is not alone. The flow of senior program managers, principal designers, applied scientists, and software engineers expelled from Big Tech is saturating the market just as hiring slows down.

Re-employment timelines reveal the new labor hierarchy:

- AI/LLM engineers: 1–3 weeks (absorbed by Anthropic, DeepMind, startups)

- Traditional software engineers: 3–6 months

- Senior program managers: 6–9 months

- Operations and middle management: 9–12 months or more

And the salary cut upon returning to work? Between $40,000 and $60,000 less for those moving from Amazon to a mid-market company.

Wall Street vs Main Street: The Great Divergence

El-Erian on PBS NewsHour summarized the phenomenon with a phrase that is becoming influential: “Wall Street vs. Main Street.” The University of Michigan Consumer Sentiment Index hit a new all-time low in May 2026, despite positive official employment data. The message is clear: macro numbers do not reflect micro suffering.

Who is suffering the most? BLS data are unforgiving:

- African American workers: unemployment rate double that of white workers

- Low-income workers: crushed by gasoline prices (post-Iran conflict oil price increases disproportionately hit low-income families, according to the Fed study published May 6)

- Women in specific sectors: information, finance, federal government

- Recent graduates: unemployment rate at 5.6%, nearly double 2019 levels

Frequently Asked Questions

Why won’t the Fed cut rates even if unemployment is low?

Because inflation at 3.3% is still double the 2% target, and with the Iran war and gasoline prices above $4.50/gallon it is expected to rise to 4%. The Fed knows that reducing rates now would further overheat the economy. It is a classic trade-off: protect purchasing power now (with high rates) vs. create unemployment tomorrow. The fed funds futures market is pricing in essentially zero cuts until April 2031.

Which sectors are actually hiring in 2026?

The engine of job growth is healthcare (+37,000 in April, +618,000 over the last 12 months), followed by transportation and warehousing (+30,000), retail (+22,000), social assistance (+17,000), and construction (+9,000). These are non-remote jobs that are difficult to automate with AI. Tech, finance, information, and the federal government are instead laying people off.

Shouldn’t AI create new jobs?

Yes, but far fewer than it destroys. The $725 billion invested in AI capex by hyperscalers in 2026 is going mainly into “steel and silicon” (data centers, GPUs, infrastructure), not personnel. The new AI jobs go to a narrow elite of specialized engineers. Meanwhile, the “information” sector has lost 342,000 jobs since November 2022, 11% of its total workforce. AI is replacing labor faster than it is creating it.

Recovery Without Victory

The April 2026 jobs report is an economic Rorschach test. Those who want to see a recovery see it: 115,000 jobs, double expectations, second consecutive month of growth, hiring recession over. Those looking beneath the surface instead see a fragile structure: an economy held up almost exclusively by healthcare, with tech in chronic erosion for 16 months, wages growing nominally but flat or negative in real terms, a Fed paralyzed by inflation, and consumer sentiment at historic lows.

As Chicago Fed President Austan Goolsbee summarized in an interview with CNBC: “The labor market has been stable for a year, a year and a half. I would characterize it as stable without being good.”

The outlook emerging from the four analyzed sources — DOL, Indeed Hiring Lab, Fortune, PBS, CNBC — converges toward a scenario of inflationary stagnation: neither a full recession nor a convincing recovery, but a prolonged limbo in which workers still have jobs but see their purchasing power eroded, companies still have liquidity but spend it on AI instead of personnel, and the Fed has the tools but not the reasons to use them.